The Buzz on Home Renovation Loan

The Buzz on Home Renovation Loan

Blog Article

Not known Factual Statements About Home Renovation Loan

Table of ContentsThe Basic Principles Of Home Renovation Loan How Home Renovation Loan can Save You Time, Stress, and Money.Home Renovation Loan Things To Know Before You BuySome Of Home Renovation LoanHow Home Renovation Loan can Save You Time, Stress, and Money.Getting My Home Renovation Loan To Work

Perhaps. In copyright, there go to the very least a pair of various ways to add improvement costs to home loans. Often lending institutions re-finance a home to gain access to equity needed to complete small renovations. If your present mortgage equilibrium is listed below 80% of the present market value of your home, and your family income sustains a bigger home loan quantity, you may qualify to re-finance your home mortgage with added funds.This enables you to complete the work required on the home with your very own funds. Then once the remodellings are total, the loan provider launches funds to you and your mortgage amount boosts. For instance, you may buy a home with a home loan of $600,000, and an improvement quantity of $25,000.

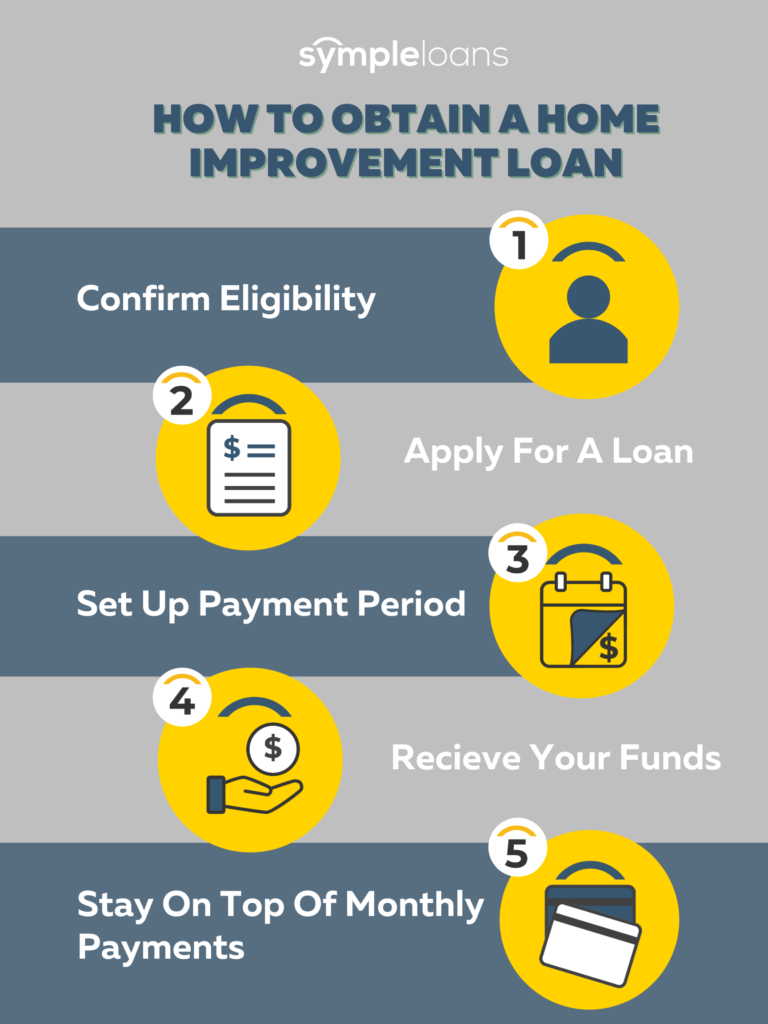

A home improvement financing can offer quick financing and versatile repayment alternatives to house owners. Home improvement finances may feature higher rates and costs for customers with negative credit rating. These financings can assist construct your credit score and increase the value of your home, yet they also have prospective downsides such as high fees and secured alternatives that put your assets in jeopardy.

Some Known Questions About Home Renovation Loan.

If you do not have outstanding credit scores, it's likely that you'll be offered high passion rates and fees if authorized.

Home enhancement lendings aren't for everybody. Elements like costs, high prices and tough credit pulls can detract from the funding's worth to you and create financial stress down the road. Not every lender charges the very same fees.

The Ultimate Guide To Home Renovation Loan

Both can be prevented. The higher your rate of interest price, the much more you will certainly have to invest each month to fund your home tasks.

Nevertheless, some fundings are protected either by your home's equity or by another asset, like a savings or investment account. If you're incapable to pay your lending and enter default, the loan provider might seize your collateral to satisfy your financial obligation. Also if a protected car loan comes with lower prices, the threat potential is much greater which's a vital aspect to take into consideration.

Increasing your credit score usage by utilizing a HELOC or debt card can also reduce your credit rating. And if you miss out on any payments or default on your financing, your loan provider is likely to report this to the credit report bureaus. Missed settlements can remain on your credit rating record for approximately seven years and the far better your credit report was in the past, the additional it will certainly fall.

Unsecured home renovation lendings generally have fast funding rates, which might make them a much better funding option than some choices. If you require to borrow a swelling sum of money to cover a task, an individual finance might be an excellent idea.

Home Renovation Loan Fundamentals Explained

Regarding 12.2. They offer some advantages in exchange - home renovation loan. Funding times are much faster, because the lending institution does not have to assess your home's value which also implies image source no closing expenses.

Like an individual lending, a home equity finance pays out one round figure you repay in fixed month-to-month payments. You set up your home as collateral, driving the interest rate down. This also might make a home equity finance much easier to get if you have inadequate credit history. However if you fail, you might lose your home.

Current ordinary rate of interest rate: Concerning 9%. As with home equity car loans, the most significant drawbacks are that you could shed your home if you can not pay what you owe and that closing costs can be expensive.

, you would certainly take out a brand-new home mortgage for even more than you owe on your residence and utilize the distinction to money your home renovation task. Shutting expenses can be high, and it might not make sense if rate of interest prices are greater than what you're paying on your present mortgage car loan.

The 7-Minute Rule for Home Renovation Loan

The optimum quantity is $25,000 for a single-family home, lower than most of your various other alternatives. You might need to give security depending on your investigate this site car loan amount (home renovation loan).

On the surface area, getting a new charge card might not appear like an excellent concept for moneying home renovations as a result of their high rate of interest prices. If you have great credit rating, you may certify for a card that provides a 0 percent introductory APR for an advertising duration. These durations normally last in between 12 and 18 months.

That makes this technique best for brief- and medium-term tasks where you have an excellent estimate of your costs. Meticulously consider the potential effect that tackling even more debt will carry your financial health. Also before contrasting lending institutions and checking out the information, perform a financial audit to ensure you can handle even more debt.

And don't fail to remember that if you squander investments that have actually increased in worth, the cash will be strained as a funding gain for the year of the withdrawal. Which implies address you may owe money when you submit your tax obligations. If you're regarding to buy a fixer upper, you can include the quantity you'll require to finance the restorations right into your home mortgage.

The 8-Minute Rule for Home Renovation Loan

Report this page